966

966“Approved”

Financial Markets Supervisory Authority

of the Republic of Azerbaijan

Resolution № 1851100014

“16” November 2018

Acting Chairman of the Management Board

______________________ Ibrahim Alishov

Regulations on assets classification and loan loss provisioning

1. General provisions

These Regulations have been developed in accordance with Article 34.2.12 of the Law of the Republic of Azerbaijan on Banks (hereinafter – the Law), and determine procedures for creation of special reserves to classify assets and cover possible losses on assets in banks and local branches of foreign banks operating in Azerbaijan (hereinafter – banks).

2. Definitions

2.0. The terms used herein shall bear the following meanings:

2.0.1. assets – loans granted by a bank, other assets allocated to be repaid, prepaid funds by a bank, assets not used in banking, investments in participation share of legal entities’ capital, and off-balance sheet liabilities;

2.0.2. outstanding amount – unpaid portion of the loan’s principal amount. The outstanding amount of the non-loan asset is its balance value;

2.0.3. total amount – total of outstanding amount of the asset and interests accrued on that outstanding amount, commission fees, delinquency charge and other unpaid amounts;

2.0.4. market price – price of goods (work, service) emerged from interaction of demand and supply;

2.0.5. liquid market – a market with sufficient sale and purchase offers, which makes the sale possible in due course and at a market price;

2.0.6. net market price- difference between the market price of an asset and all its sale related costs;

2.0.7. consumer loan – loans to individuals for purposes not related to entrepreneurship or professional activity, acquisition and construction of real estate;

2.0.8. business loan – loans to legal entities and unincorporated individual entrepreneurs for entrepreneurial purposes;

2.0.9. restructured assets – debt liability, contractual terms of which were changed, or which was documented as a new obligation with a view to implement the debt liability, due to debtor’s financial difficulties. An asset is considered to be a restructured asset if the contract provides for a different repayment schedule in the event of a financial difficulty of the borrower and such a case takes place. The following is provided for under changing contractual terms:

2.0.9.1. decrease in interest rate;

2.0.9.2. decrease in principal amount or accrued interest;

2.0.9.3. extension of maturity;

2.0.9.4. issue of new or additional grace period (non-repayment within a specified period or only interest payments);

2.0.9.5. change of a payment schedule of principal and interest;

2.0.9.6. waiver of collateral or its replacement with a lower value collateral;

2.0.9.7. In addition to those specified in sub-items 2.0.9.1-2.0.9.6 herein, provision of more favorable rights and advantages than existing contractual terms to the customer by a bank.

2.0.10. overdue loan – a loan where payments against the principal amount or interest accrued, or the outstanding portion of any of them, are delinquent for more than 30 calendar days beyond the contractual maturity date;

2.0.11. collateral – an asset pledged as collateral, mortgage and other types of collateral to ensure performance of liabilities by the borrower or a third party;

2.0.12. special reserves (hereinafter – reserves) – funds allocated to cover possible asset losses;

2.0.13. interbank claims - deposits placed by a bank with another bank, correspondent account balances and granted loans;

2.0.14. joint group of borrowers –persons who act as mutual guarantors for repayment of the loan received by each member of the group under the agreement;

2.0.15. the debt-to-income (DTI) ratio – the ratio of borrower’s monthly debt burden on consumer loans to his/her income (on individuals in a group of joint borrowers the ratio of their total monthly debt burden to their total income);

2.0.16 debt burden - total amount of unpaid liabilities of the borrower (including credit lines) on loans taken from credit institutions, total amount of monthly repayments determined by the schedule (including credit lines) where he/she acted as a guarantor, as well as monthly repayments on leasing agreements and other debt liabilities on the basis of information from credit bureaus;

2.0.17. monthly installment – monthly repayment provided by the loan repayment schedule in the loan agreement (monthly repayment on credit lines and loans not provided for in the loan agreement is calculated on an annuity basis based on its total amount and the period left until the end of the agreement);

2.0.18. borrower's income – monthly income of an individual borrower at least for recent 6 (six) months approved with relevant documents (certificate of employment with salary, certificate of scholarship from an educational institution, certificate of payment of pensions and benefits to the borrower by social security authorities, bank reference confirming interest income on borrower's existing deposit accounts or excerpts from the account confirming fixed income domestically). If the documents confirming borrower's income indicate other periodic income instead of monthly income, monthly income is calculated by dividing that income by the number of months in the period;

2.0.19. non-hedged borrower – sensitive to exchange rate risk arising or likely to arise from any form of liability in a foreign currency (income not in the same foreign currency);

2.0.20. acceptable collateral – the following types of collateral for purposes of these Regulations:

2.0.20.1. government securities of the Republic of Azerbaijan, as well as securities, government guarantee or the guarantee of the Central Bank issued by the Central Bank of the Republic of Azerbaijan (hereinafter – the Central Bank);

2.0.20.2. the national currency of the Republic of Azerbaijan, bank metals or currency of countries of the Organization for Economic Cooperation and Development (OECD) with a minimum investment rating issued by international rating agencies (Standard & Poor's, Fitch Ratings, Moody's, hereinafter - international rating agencies) pledged to the bank;

2.0.20.3. backed securities issued by the Mortgage and Credit Guarantee Fund of the Republic of Azerbaijan;

2.0.20.4. securities and guarantees issued by multilateral development banks with minimum investment rating issued by international rating agencies;

2.0.20.5. securities and guarantees issued by governments and central banks of OECD countries with minimum investment rating issued by international rating agencies;

2.0.20.6. securities and guarantees issued by banks registered in OECD countries with a minimum investment rating issued by international rating agencies, as well as banks operating in the Republic of Azerbaijan with a credit rating issued by international rating agencies with a maximum of 1 (one) step below the country's (sovereign) debt rating;

2.0.20.7. securities and guarantees issued by financial institutions registered in OECD countries with a minimum “A-” credit rating (or equivalent) issued by international rating agencies.

2.0.21. multilateral development banks - an international financial institution established by two or more countries to support economic development;

2.0.22. secured asset – asset not less than 100% (one hundred) of the amount of liability secured by its market value if the collateral is acceptable, and not less than 150% (one hundred fifty) if the collateral is not acceptable;

2.0.23. unsecured asset – asset secured by securities and guarantees, where collateral is acceptable whose market value is not more than 100% (one hundred) of the amount of liability, where collateral is not acceptable, is less than 150% (one hundred fifty), or the collateral of which is issued by resident and non-resident legal entities that do not have the minimum investment rating issued by international rating agencies.

3. Classification of assets

3.1. Banks classify and create reserves on their assets under these Regulations and their internal procedures. Internal procedures set regulation and recording of assets classification, analysis criteria of asset quality and control procedures, as well as procedures to write off loss assets from the balance sheet.

3.2. Assets are classified by a responsible structural division, designated by bank’s internal procedures based upon the principle of avoiding the conflict of interests.

3.3. Assets are divided into standard and non-standard assets. Standard assets include satisfactory and watch assets, non-standard assets include non-satisfactory, doubtful and loss assets.

3.4. Assets are classified on the delinquency period and quality criteria. If as a result of the two classifications, classification categories for an asset differ, the lower category is used. Satisfactory assets are the highest and loss assets are the lowest category. Satisfactory assets are classified as high, while loss assets as low-quality assets.

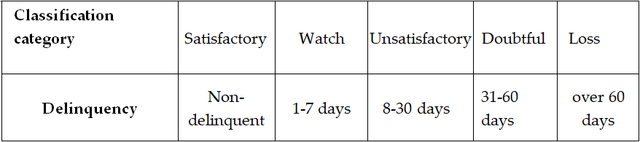

3.5. Classification of assets by delinquencies:

3.5.1. Unless otherwise provided herein, classification category in terms of delinquency is determined in accordance with the following table:

3.5.2. where collateral is acceptable, if the market price of asset collateral falls below 100% (hundred) of asset’s total value; where collateral is unacceptable, falls below 150% (one hundred fifty) of the asset’s total amount, secured assets are classified on delinquency days set for unsecured assets;

3.5.3. asset’s delinquency period (on principal and interest debts) is calculated from the date set for repayment of principal and/or interest debts in the relevant agreement.

3.6. Assets are classified in terms of quality on the criteria set below. Discovery of one or more of the criteria (cases) established per classification category gives grounds for attributing the asset to that classification category. A lower classification category is used when cases relating to different classification categories for the same asset are identified.

3.6.1. criteria on satisfactory assets:

3.6.1.1. when principal and interest repayments are fully commensurate with borrower's cash income and financial condition.

3.6.2. criteria on watch assets:

3.6.2.1. when, after the placement of the asset, there are circumstances that pose a potential risk to the borrower's financial condition in his/her activity area;

3.6.2.2. in case of non-submission of periodic reports specified in the contract (e.g., balance sheet, income statement, etc.);

3.6.2.3. if a foreign currency denominated loan is issued to a non-hedged borrower.

3.6.3. criteria on non-satisfactory assets:

3.6.3.1 negative circumstances in borrower's creditability (more than 30 day delinquency twice over recent 6 months) as a result of changes in economic conditions (negative zoning of real GDP growth rate, as well as inflation above the Central Bank's target or year-over-year unemployment increase by more than 20%);

3.6.3.2. when there is a need for additional sources for debt repayment (e.g., additional collateral, sale of property, attraction of additional funds by the borrower, etc.);

3.6.3.3. if documents confirming use of the loan for its intended purpose are not submitted;

3.6.3.4. if there are significant delays in the schedule of work specified in the loan agreement or business plan that is a part of the loan agreement;

3.6.3.5. when one or more of other assets of a borrower or a group of related borrowers in the same bank are classified as non-standard assets. This criterion applies when the sum of non-standard assets of a borrower or a group of related borrowers is at least 20% (twenty) percent of his/their total liabilities;

3.6.3.6. in the event of bankruptcy of one of the companies with a qualifying holding in the group of related borrowers to which the borrower belongs;

3.6.3.7. if the borrower has been operating with loss for more than 1 (one) year;

3.6.3.8. when the periodicity of interest repayments under contractual terms is more than 90 days (a provision is created for such assets under the relevant classification rate without applying the case specified in Item 11.2 herein).

3.6.4. criteria on doubtful assets:

3.6.4.1. when the bankruptcy process of the borrower begins;

3.6.4.2. if credit files do not contain documents related to the loan assessment.

3.6.5. criteria on loss assets:

3.6.5.1. when the borrower is declared bankrupt or terminates entrepreneurial activity;

3.6.5.2. if the borrower dies, is considered dead or missing in accordance with the Civil Code of the Republic of Azerbaijan, or it is impossible to find the borrower who failed his/her liabilities (when search operations started on the person in accordance with the Law of the Republic of Azerbaijan on Search Operations);

3.7. Analysis of quality criteria is documented. In this case, findings of internal models adopted by Supervisory Boards of banks, as well as findings obtained from monitoring reports are also included in the documentation of the analysis.

3.8. Non-standard asset’s classification category can be upgraded to a watch asset if:

3.8.1. overdue principal and interest on the asset is repaid in full (excluding repayments at the expense of collateral);

3.8.2. the borrower does not have another overdue loan, which makes up more than 20% of his/her total liabilities, in the same bank;

3.8.3. borrower’s quality criteria are not lower than limits set in sub-item 3.6.2 herein.

3.9. To classify a non-standard asset as a satisfactory asset, in addition to the requirements set in sub-items 3.8.1 and 3.8.2 herein, at least 3 (three) consecutive payments on the annuity schedule should be made in full and on time, as well as the requirements of sub-item 3.6.1 herein should be met. In this case, repayments with a deviation of up to 10 (ten) days from the repayment schedule are considered as timely repayments.

4.Creation of reserves and loss asset charge off

4.1. Reserves are created for possible asset loss provisioning and are divided into two categories:

4.1.1. general reserves created to cover possible losses on bank's standard assets;

4.1.2. specific reserves created to cover possible losses on bank's non-standard assets.

4.2. Unless otherwise provided herein, the rates of reserves by classification categories are determined in accordance with the following table.

4.3. Reserves are created on total asset amount in the national currency of the Republic of Azerbaijan against the bank’s expenses.

4.4. If the principal amount or interest payments on the asset are delinquent for over 90 days, reserves are created to 100% of accrued interests.

4.5. Reserves are created per asset or, through assessment of risks inherent to an assets group, on this group (loans, interbank claims, securities, payables, and other assets). Created reserves are used to cover possible losses on all assets of that group.

4.6. Loss asset is charged off from the balance sheet in the amount of the reserve created on that asset).

4.7. The bank charges off loss assets from the balance sheet at the decision of the Supervisory Board based upon the petition of the Management Board. All assets charged off from the balance against reserves and outstanding interests on these assets are recorded and maintained in relevant off-balance sheet accounts (sub-accounts) for at least 5 (five) years. When creating reserves for loss assets, the discounts specified in Section 11 herein do not apply to assets written off and subsequently returned to the balance sheet.

4.8. No provision is made on correspondent accounts with the Central Bank and the banks with the minimum investment rating issued by international rating agencies and registered in OECD countries, as well as on other claims with no delinquency due to the Central Bank and banks with a minimum “AA-” credit rating (or equivalent) registered in OECD countries.

4.9. Created reserves are assessed in terms of adequacy to asset quality by the structural division, that carry out the classification, at least once a month, no later than the last business day of a month. The quality criteria are assessed at least once every 6 (six) months for borrowers with total residual debt of more than 3% (three) of Tier I capital in the same bank, and at least once a year for other borrowers, unless otherwise provided herein.

4.10. For the purposes of prudential reporting the following is taken into account:

4.10.1. if monthly asset evaluation identifies quality improvements, reserves already created, and funds received by the bank later on repayment of assets previously charged off from the balance sheet are channeled to reduce the relevant expenses account, and charged to income if the expense account has no balance left;

4.10.2. the amount of specific reserves created for any asset is deducted from that asset’s amount. The amount of the general reserve created for an asset is recorded as a separate item under the ‘Capital’ accounts;

4.10.3. the reserve account may not have a debit balance. If assets to be charged-off against reserves exceed the balance of the reserve account, the required amount is provided from the everyday operating cost. Reserves may not be funded from the ‘Retained Earnings’ or other capital accounts.

5. Consumer loan classification

5.1. Consumer loans are classified as follows:

5.2. Consumer loans are classified as non-satisfactory at the time of placement if:

5.2.1. the borrower has an overdue loan over recent 6 (six) months;

5.2.2. difference between total income of the borrower or members of the joint group of borrowers and the debt burden is less than the subsistence level in the country (is calculated as per Annex 1 herein);

5.2.3. the period of interest payment under contractual terms is more than 90 days, except for loans issued on the basis of life insurance (a provision is created for such assets under the relevant classification rate without applying the case specified in Item 11.2 herein);

5.2.4. the DTI ratio is over 45%, except for the following cases (the DTI ratio on consumer loans is calculated as per Annex 2 herein):

5.2.4.1. the loan to value ratio (hereinafter – the LTV ratio) is not over 90%, in case foreign currency denominated deposits in the same bank (belonging to the borrower or a third party) or bank metals pledged (held) to the bank act as collateral for consumer loans in foreign currency;

5.2.4.2. if the LTV ratio is not over 90%, when deposits in the same bank (belonging to the borrower or a third party) and bank metals pledged (held) to the bank act as collateral for consumer loans in the national currency;

5.2.4.3. if the LTVratio is not over 70%, when precious metals (except for bank metals) pledged (held) in the bank act as collateral for consumer loans in the national currency.

5.3. When one or more of other assets of a borrower or a group of related borrowers in the same bank are classified as non-standard, the consumer loan is classified as an unsatisfactory asset. This requirement applies when total non-standard assets of one borrower or a group of related borrowers makes up at least 20% (twenty) of his/their total liabilities.

5.4. If the borrower dies, is considered dead or missing in accordance with the Civil Code of the Republic of Azerbaijan, or it is impossible to find the borrower who failed his/her liabilities (when search operations started on the person in accordance with the Law of the Republic of Azerbaijan on Search Operations) the consumer loan is classified as a loss loan.

5.5. Sub-items 3.6.1.1, 3.6.2.1, 3.6.3.1, 3.6.3.2, 3.6.3.4 and 3.6.5.1 herein are assessed at least once a year for borrowers whose total outstanding debt in the same bank exceeds 1 (one) percent of Tier I capital and are classified as per Section 3 herein.

6. Restructured assets classification

6.1. The asset’s previous classification category may not be improved at the time of asset’s restructuring.

6.2. Upon restructuring, the asset classification category may be improved as follows:

6.2.1. assets with payments to be made in monthly installments under contractual terms – if there is no delay in installment payments within 6 months;

6.2.2. Consumer loans can be upgraded to the maximum unsatisfactory category if there are no delays in payments within six months, and to the maximum watch assets if there are no delays in payments within twelve months.

6.2.3. Interbank claims, as well as assets with payments to be made in quarterly, semi-annual and annual installments, and in other intervals under contractual terms – provided that at least 50% of the asset’s principal amount is repaid and liabilities on the principal amount and accrued interests are implemented in due time and fully

6.3. In light of the requirements of Items 6.1 and 6.2 herein, the classification category of the assets restructured until 23 February 2015 may be improved at most up to non-satisfactory, while assets restructured after 23 February 2015 at most up to watch assets.

6.4. When determining the asset’s classification category upon restructuring, the asset’s quality criteria should be considered along with the requirements of Items 6.2 and 6.3 herein.

7. Classification of interbank claims

7.1. Interbank claims are classified as follows:

7.2. If the bank license is revoked in a forced order or bankruptcy proceedings specified in the Law are initiated with respect to the bank, interbank claims are classified as loss assets.

8. Classification of investments in securities and equity investments

8.1. For classification purposes, securities (except for foreclosed securities) are divided into three categories: highly, moderately and lowly liquid securities.

8.2. For the purposes hereof, highly rated securities include government securities of the Republic of Azerbaijan, securities issued by the Central Bank of the Republic of Azerbaijan, backed securities issued by the Mortgage and Credit Guarantee Fund of the Republic of Azerbaijan, as well as securities issued in OECD countries with a minimum ‘AA-‘ credit rating (or equivalent) issued by international rating agencies.

8.3. No reserves are created, if investments are made to highly liquid securities.

8.4. Moderately liquid securities include:

8.4.1. securities entered to the first level quotation sheet or priced daily by the Baku Stock Exchange;

8.4.2. securities not attributable to high quality securities issued in OECD countries with a minimum investment rating given by international rating agencies;

8.4.3. securities that have not received any rating, about the financial state of the issuer of which the bank has sufficient information.

8.5. When investing to moderately liquid securities, they are classified as specified in Section 3 herein.

8.6. Lowly liquid securities include securities, rated by international rating agencies below investment rating or not rated at all and securities, about the financial state of the issuer of which the bank has no sufficient information.

8.7. The portion of carrying value of lowly liquid securities, below their market price is classified as an unsatisfactory asset, while the portion above their market price as a loss asset.

8.8. No reserves are created on securities recorded in bank’s aggregate income statement (P&L statement) on a daily basis.

8.9. Equity investments are classified under the quality criteria prescribed in Item 3.6 herein. No reserves are created on the type of assets classified as satisfactory. If legal entity's operations are suspended or terminated, the equity investment is categorized as a loss asset.

9. Classification of assets (properties) not used in banking

9.1. From the date of foreclosure other real estate owned (OREO) property not used in banking are classified and provisioned accordingly as follows:

9.1.1. if the market price of real estate is above its book value, it is carried at the book value as an unsatisfactory asset at a minimum;

9.1.2. if the market value of real estate is below its book value, it is carried at the market value as an unsatisfactory asset at a minimum, whereas difference is recognized as loss asset.

9.2. The OREO and fixed assets previously used by the bank may not be recorded in the balance sheet from the date they are not used for over 2 (two) years. Upon completion of the relevant period the real estate is charged off from the balance and recorded in an off-balance sheet account.

9.3. Repossessed movable property, including securities, and movable property not used in banking from the date of repossession are classified and provisioned accordingly as follows:

9.3.1. if the market value of movable property is above its book value, it is classified at a minimum as an unsatisfactory asset at the book value within 60 days;

9.3.2. if the market value of movable property is below its book value, it is classified at a minimum as an unsatisfactory asset at the market value within 60 days, whereas difference is recognized as a loss asset;

9.3.3. repossessed movable property is classified at a minimum as a doubtful asset after expiry of the 60 day period;

9.3.4. repossessed movable property is classified as loss assets, charged-off, and recognized in a relevant off-balance sheet account after expiry of a 120 day period.

10. Classification of off-balance sheet liabilities

10.1. Off-balance sheet liabilities are divided into 2 groups for classification purposes:

10.1.1. Group 1 – entitles the bank to not fulfill its liabilities fully or partially under the contract unilaterally;

10.1.2. Group 2 – the liability is executed unconditionally.

10.2. Off-balance sheet liabilities are classified on balance sheet assets, as defined herein, with the consideration of the following:

10.2.1. Group 1 off-balance sheet liabilities – from the date the off-balance sheet liability is transferred to balance sheet accounts;

10.2.2. Group 2 off-balance sheet liabilities– from the date the off-balance sheet liability is created;

10.2.3. guarantees (warranties), and letters of credit issued by the bank are classified at a minimum as watch assets from the moment they are recognized on the balance sheet.

11. Role of securitization in creating reserves on loss assets

11.1. Securitization on assets are divided into 5 (five) groups to be considered in loan loss provisioning:

11.1.1. Group 1 securitization:

11.1.1.1. If the bank blocks the funds in the borrower's deposit account in national and freely convertible currency in equal parts to the asset and the bank has the right to write off the funds without the account holder's order under the agreement (if the borrower's payment on the asset is delinquent for more than 30 (thirty) days and credit is not repaid against the deposit, the said asset is classified and provisioned as per relevant items herein);

11.1.1.2. government securities of the Republic of Azerbaijan, as well as securities issued by the Central Bank, state guarantee or guarantee (warranty) of the Central Bank;

11.1.1.3. backed securities and guarantee issued by the Mortgage and Credit Guarantee Fund of the Republic of Azerbaijan;

11.1.1.4. securities and guarantees issued by governments or central banks of OECD countries with the minimum ‘A-’ country (sovereign) debt rating (or equivalent) issued by international rating agencies;

11.1.1.5. bank metals pledged (vault) to the bank;

11.1.1.6. securities and guarantees issued by multilateral development banks with the minimum ‘A-’ credit rating (or equivalent) given by international rating agencies;

11.1.1.7. securities and guarantees issued by banks registered in OECD countries with a minimum “AA-” credit rating (or equivalent) issued by international rating agencies.

11.1.2. Group 2 securitization:

11.1.2.1. precious metals pledged (vault) to the bank (except for bank metals);

11.1.2.2. guarantees (warranty) issued by the banks operating in the Republic of Azerbaijan;

11.1.2.3. securities and guarantees not attributable to Group 1 securitization issued by governments or central banks of OECD countries with minimum investment ratings issued by international rating agencies;

11.1.2.4. securities and guarantees not attributable to Group 1 securitization issued by multilateral development banks with minimum investment ratings issued by international rating agencies;

11.1.2.5. securities and guarantees not attributable to Group 1 securitization issued by banks registered in OECD countries with minimum investment rating issued by international rating agencies;

11.1.2.6. securities traded on the Baku Stock Exchange or issued by companies registered in OECD countries with a minimum ‘A’ credit rating (or equivalent) issued by international rating agencies;

11.1.3. Group 3 securitization:

11.1.3.1. real estate.

11.1.4. Group 4 securitization:

11.1.4.1. vehicles.

11.1.5. Group 5 securitization:

11.1.5.1. other collateral not included to the previous groups.

11.2. If Group 1 securitization acts as asset collateral, no provision is made for the unconditionally secured portion of the asset.

11.3. Group 2, 3 and 4 securitization are considered only on provisioning on loss assets. In this case, net market price of securitization is considered under the following conditions:

11.3.1. net market price considered in calculation should not exceed total asset amount;

11.3.2. bank’s rights over collateral are documented under the legislation;

11.3.3. maturity of collateral may not be less than that of the liability it secures;

11.3.4. there should be a liquid market to sell the collateral;

11.3.5. the value of the collateral should be revalued;

11.3.6. the security’s market price should be set by independent appraisers.

11.4. If the terms in Item 11.3 herein are met, reserves on loss assets are calculated as follows:

E = A – Lx i

where: E – reserve amount, A – total asset amount, L - liquid value of the security recognized, i – coefficient corresponding to securitization group for calculation of collateral’s liquid value.

11.5. The liquid value of securitization is determined as follows:

11.5.1. Group 2 – 40% of the net market price;

11.5.2. Group 3 – 30% of the net market price;

11.5.3. Group 4 – 20% of the net market price;

11.5.4. Group 5 securitization is not considered in creating reserves.

11.6. If realization of collateral is not completed within 3 (three) years after the asset is included in the loss assets category, a reserve of 100% is created for those assets.

12. Final provisions

These Regulations take effect six months after being published on electronic version of the State Register of Legal Acts of the Republic of Azerbaijan.

Annex 1

to the Regulations on assets

classification and loan loss provisioning

Calculation of the difference between income of a borrower or members of a joint group of borrowers and debt burden

where,

I – borrower’s net income after taxes,

D – borrower’s debt burden,

PMT – monthly repayment on a new loan,

n(n=1,2,...) – the number of joint borrowers,

SM – subsistence level indicator set on the country with the relevant law of the Republic of Azerbaijan on the relevant year .

Annex 2

to the Regulations on assets

classification and loan loss provisioning

Calculation of the debt-to-income ratio

where,

BGN – debt-to-income ratio,

D – borrower’s debt burden,

PMT – monthly installment on a new loan,

I – borrower’s net income after taxes,

n (n=1,2,...) – the number of the members of a joint group of borrowers.