966

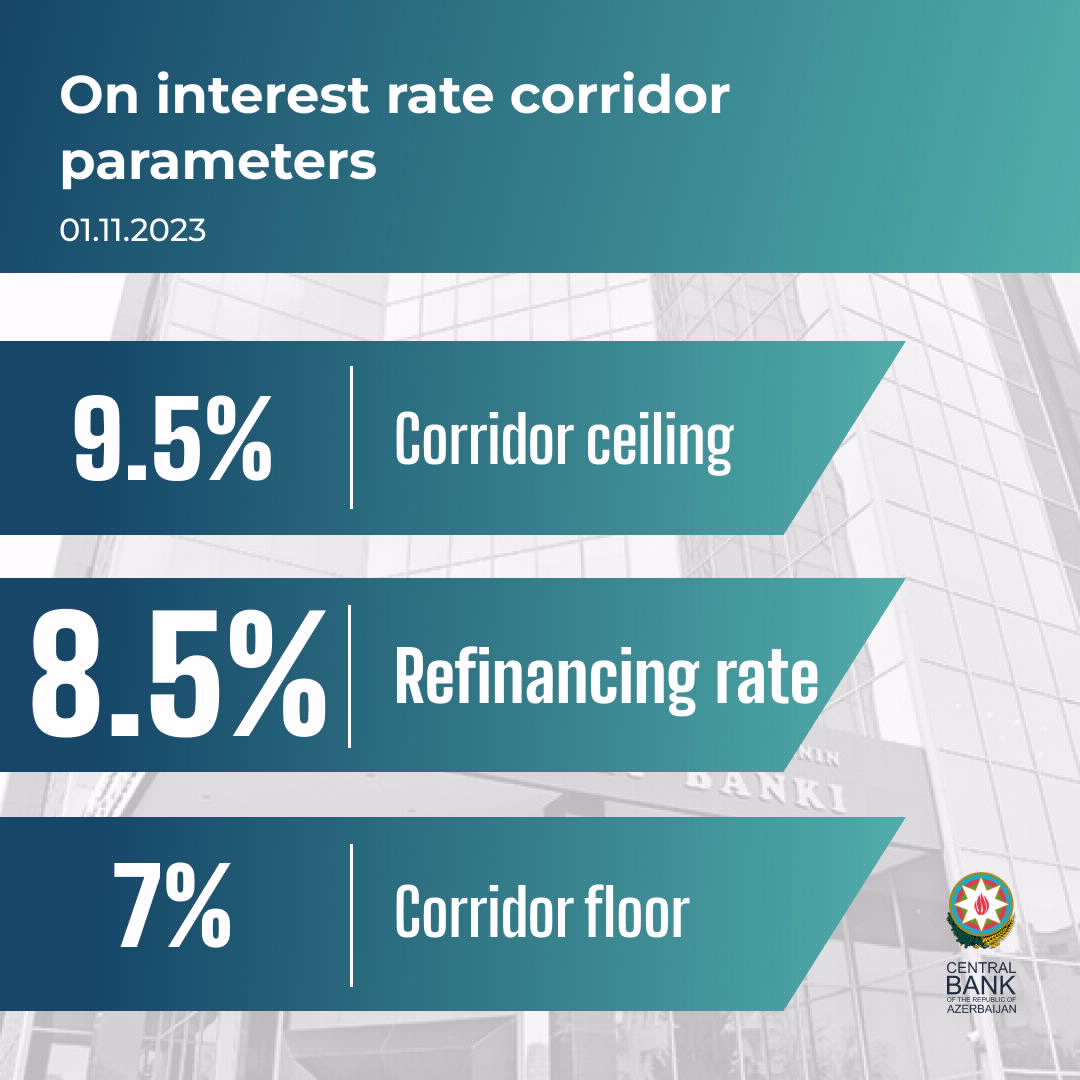

9661 November 2023, Baku: The Management Board of the Central Bank of the Republic of Azerbaijan decided to decrease the refinancing rate to 8.5% from 9%, the floor of the interest rate corridor to 7% from 7.5% and the ceiling of the interest rate corridor to 9.5% from 10%.

This decision was made considering the change in internal and external inflation factors, as well as considerable prevalence of supply over demand in the FX market.

The downward trend of annual inflation rate has been continuing since the last meeting dedicated to the monetary policy. In September 2023 annual inflation decreased to 5.1%, which is within the target band (4±2%). The annual inflation rate is more than three times below the annual inflation last September (15.6%). The annual core inflation rate also decreased to 5.2% in September.

The dynamics of annual inflation dropped in response to external factors and the anti-inflationary policy pursued. Persistent drop in global commodity, in particular, food prices, approximation of international transportation costs to the pre-pandemic level, the tight monetary policy implemented in trade partners and the appreciation of the nominal effective exchange rate had a downward effect on imported inflation. According to the World Bank, the total commodity price index decreased by 19.8% on annual in September, by 25.6% on energy and by 3.9% on non-energy prices. While according to the UN FAO, the food price index decreased by 10.7% annually in September. On the backdrop of the equilibrium in the domestic FX market, the nominal effective exchange rate of the manat appreciated by 21.6% over 10 months of 2023. Analyses suggest that this factor was the key in containing the imported inflation. At the same time, efforts of the Government, including the implementation of the measures specified in the Decree of the Cabinet of Ministers ‘on Additional measures to strengthen the monitoring of inflation and prices’ are driving inflation down.

Amid the foreign trade surplus ($13.9B over 9 months) supply prevailed over demand at 99% of forex auctions held by the Central Bank since early year. Accordingly, the Central Bank made $1247.9M worth purchase-oriented interventions to the FX market over 10 months. FX reserves of the Central Bank increased by 16.8% ($1.5B) to $10.5B over 10 months.

The Central Bank continues the anti-inflationary monetary policy and measures oriented towards expanding capabilities to affect inflation. Monetary policy tools are applied considering the liquidity position of the banking system and the balance of risks. Maintenance of required reserves under the new norms since August, elimination of the daily limit on liquidity absorbing standing facilities and regular auctions with various duration notes minimized excess liquidity in the banking system. In general, the size of the Central Bank’s sterilization portfolio (including required reserves in the manat and liquidity absorbing standing facility) has increased by AZN3.9B to AZN6.4B since the launch of the new monetary policy framework (beginning of September 2022). Over 10 months average weighted interest rates on deals in the national currency both in the secured and unsecured interbank money market responded to the change of the interest rate corridor. For the first time in the country interbank repo interest rates were within the interest rate corridor of the Central Bank, which can be exemplified as a great achievement. Hence, in October the one-week interbank repo interest rate (1W AINAIB) stood at 8.38%, which is within the interest rate corridor.

Despite the drop in actual inflation, some uncertainties related to the external environment of inflation across the forecast horizon linger. Geopolitical tension, emergence of new points of war, natural anomalies may push food and energy prices up in the world market. International organizations revised up energy price forecasts for 2024, likely to weigh on inflation rates in energy importing partner countries.

The main internal risk, likely to weigh on inflation, is overexpansion of demand. In the case supply prevails over demand in FX market over the remaining period of the current year the Central Bank may further increase purchase-oriented interventions to the FX market, which may lead to double-digit (over 20%) increase in money supply. While increase in base money may push inflation upcoming years. The decision on Central Bank intervention and policy easing will serve to avoid the appreciation of the manat within the current stable exchange rate regime.

In general, stronger downward factors in the inflation environment and stabilized inflation expectations allow the annual inflation to be within the target band as of the end of the current year and in 2024. According to October forecasts of the Central Bank inflation is expected to be within the target band in the medium-run – annual inflation is forecast to stand at 4.3% as of end-2023, 5.3% in 2024 and 3.4% in 2025. In several consecutive forecast updates this year, inflation forecasts for 2024 and 2025 were within the target band.

The Central Bank will make next monetary policy decisions considering the comparison of the forecast inflation with the target and updated macroeconomic forecasts. The Bank will consider options for stepwise policy easing in the event the above risks related to external and internal environments do not materialize and the pressures of the appreciation of the manat do not subside.

This decision takes effect on 2 November 2023. The next decision related to the monetary policy will go public on 20 December 2023.

01.11.2023