966

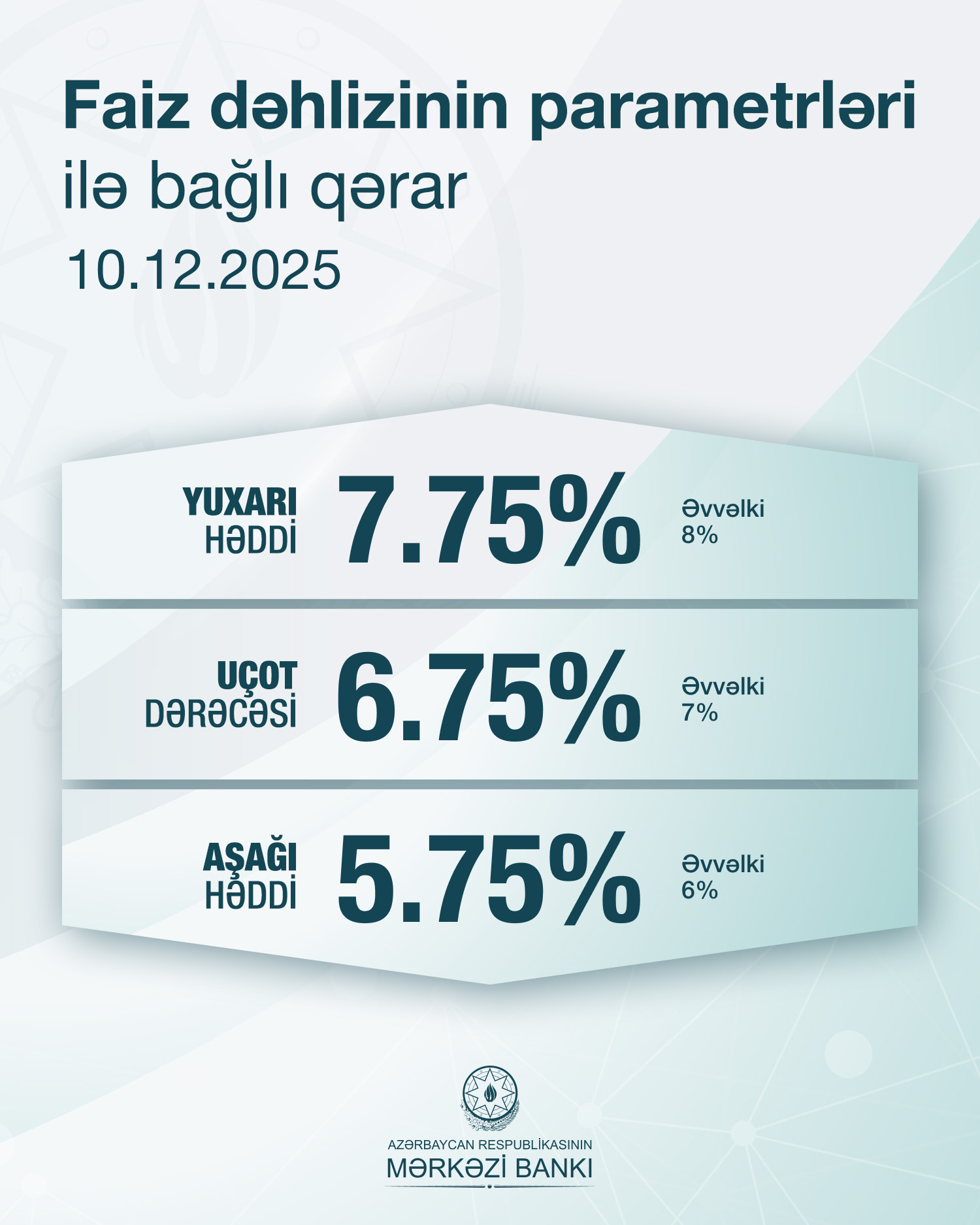

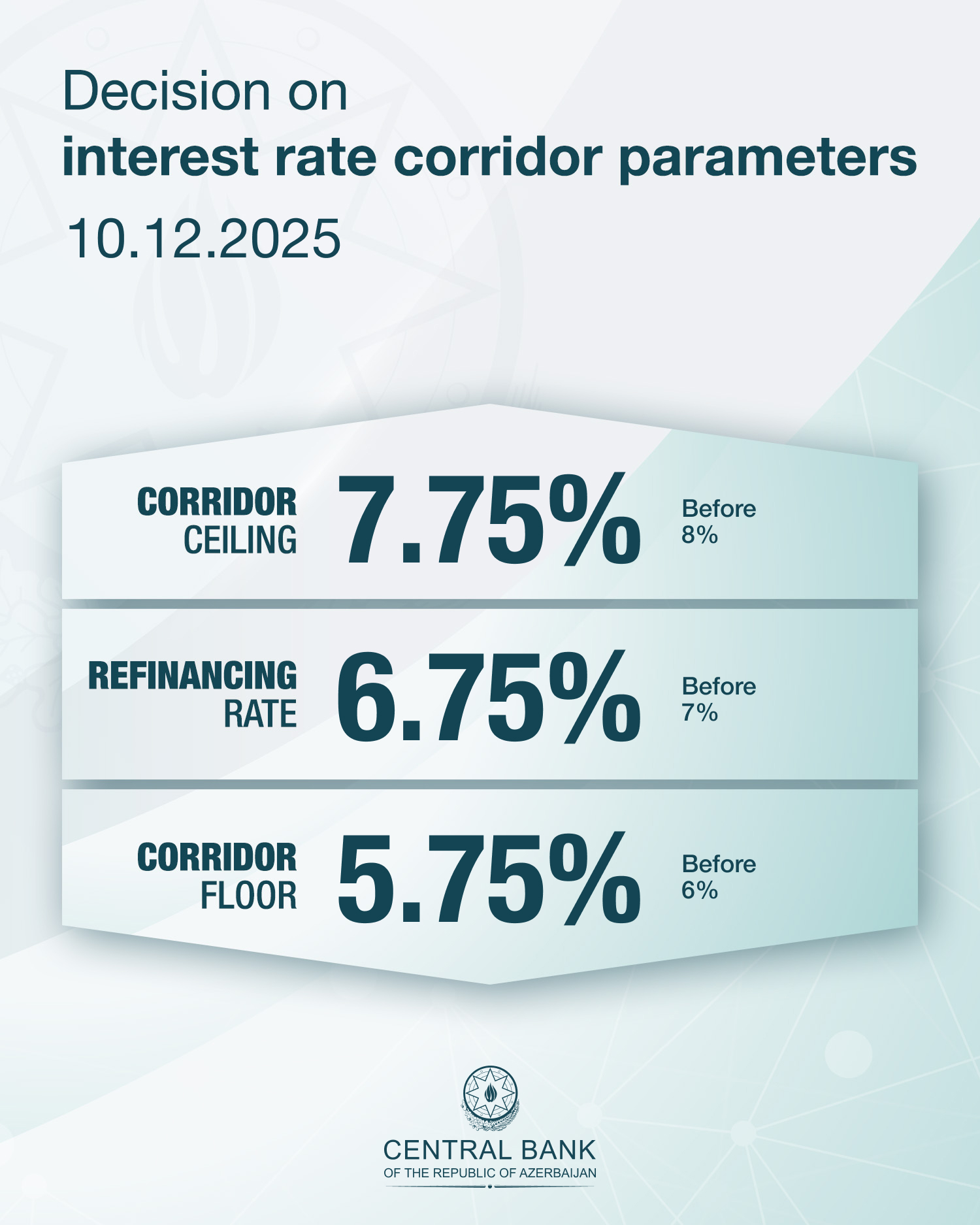

96610 December 2025, Baku: The Management Board of the Central Bank of the Republic of Azerbaijan has decided to lower all parameters of the interest rate corridor by 0.25 percentage points - the refinancing rate has been reduced to 6.75%, the floor of the interest rate corridor to 5.75%, and the ceiling to 7.75%.

The decision has been made considering the alignment of actual inflation with the forecasted target range (4±2%), the current stance of global economy and financial markets, domestic macroeconomic developments, and the transmission of monetary policy decisions to the real sector.

Presently, annual inflation is aligning with the projected trajectory and is within the target band. In October 2025, 12-month inflation stood at 5.9%, while annual price increases were 8.2% for food products, alcoholic beverages, and tobacco products, 5.6% for paid services, and 2.5% for non-food items. Annual core inflation stood at 5%. Actual inflation was driven by external and domestic cost factors.

The FX market remains stable, with overall supply exceeding demand. In January-November 2025, foreign currency purchase operations by currency exchange points have exceeded sales operations by $393M. Dollarization of resident individuals’ savings has decreased by 2.1 percentage points over the past 12 months to 29% in November, reflecting optimistic exchange-rate-related expectations. On this backdrop, over 11 months of 2025 foreign exchange reserves of the Central Bank increased by 4.3% to $11.4B.

The key factor of the FX market equilibrium – the external sector indicators remain favorable. Over 9 months current account surplus of the balance of payments amounted to $3B (5.4% of GDP), driven by surplus of foreign trade and secondary income balances. The dynamics of net receipts on remittances, the key component of the secondary income balance, is positive year-over-year. The Central Bank’s projection that the current account will continue into 2025 and 2026 remains unchanged.

Monetary policy tools are applied in response to financial market developments and changes in banking system liquidity. The Ministry of Finance’s ongoing deposit auctions continue to exert upward pressure on banking system liquidity. Since the last meeting, interest rates in the unsecured money market have remained within the Central Bank’s interest rate corridor, close to the refinancing rate. The average daily rate of the AZIR index was 6.89% in October, 6.91% in November, and 6.94% over the past period of December. The Central Bank has minimized the effect of autonomous factors on AZIR with its one-week open market operations. The yield curve and yields on Central Bank notes have declined since the last meeting. Deposit and credit interest rates have not undergone considerable changes since that time.

Under the baseline scenario, the forecast that annual inflation will be within the target range at end-2025 and in 2026 remains unchanged. However, the analysis of recent developments indicates that the inflation forecast is likely to be revised downward next year.

The analysis of changes in the balance of inflation risks since the last meeting suggests that upside risks have relatively subsided. However, geopolitical tensions and instability in the global trade environment continue to keep uncertainties in commodity and financial markets elevated. The key external risk factor relates to the transmission of import prices to domestic inflation, which will depend on inflation in trade partner countries and the dynamics of the nominal effective exchange rate. Domestic risk factors are driven primarily by supply- and cost-related pressures. The initial parameters of the 2026 state budget, together with a slowdown in the annual growth of loans reduce the risk of aggregate demand overheating.

Decisions regarding the parameters of the interest rate corridor will depend on the dynamics of forecasted and actual inflation, as well as updated results of macroeconomic analyses. The Central Bank will continue to employ all available tools to ensure price stability.

This decision takes effect on December 11, 2025. The schedule for the disclosure of decisions in 2026 related to the interest rate corridor parameters will be published by the end of this year.

10.12.2025